Now Playing: Health Care. Referendum 67 Washington State Ballot

Topic: State & Local

Picked up the mail yesterday which included a letter from my local agent who writes my auto and homeowners insurance.

Although it is on a letter bearing his personal agency letterhead, he didn't write the letter and he didn't sign it. His insurance company wrote it and no doubt told him what to say and how to say it. Among other things it says,

"Washington's trial lawyers sponsored a self-serving bill in the state Legislature this year that will significantly increase frivolous lawsuits ..."

According to Dictionary.com,

frivolous lawsuits would be

"characterized by lack of seriousness or sense: as in frivolous conduct."

They would be lawsuits that are

"self-indulgently carefree; unconcerned about or lacking any serious purpose."

These would be lawsuits filed by self-serving trial lawyers on behalf of persons

"given to trifling or undue levity: as in a frivolous, empty-headed person."

Oh! And these would be lawsuits

"of little or no weight, worth, or importance; not worthy of serious notice: as in a frivolous suggestion."

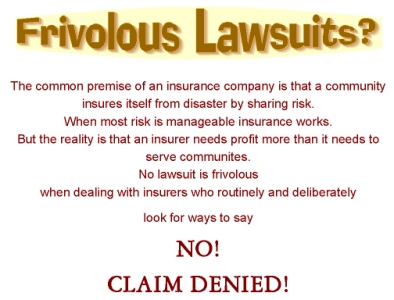

Now given the seriousness of the situation (I assume it to be serious enough that the State Legislature might have been on to somebody) do we not need to learn more about these notorious and rampant frivolous lawsuits?

Or are we to believe that the wise folks behind "Reject 67" consider themselves absolutely smarter than 60% of the State Legislature as well as 100% of those of us who voted them into office?

My auto/homeowner insurance agent has passed on to me a threat from his casualty company. And I quote,

Passage of R-67 will increase insurance rates for every person and business that purchases insurance in Washington

Would I be remiss in not taking that as a threat from my insurance company? If R-67 passes, my rates will go up?

So I should vote against R-67 or else?

I also received a flyer from "Consumers Against Higher Insurance Rates" telling me R-67 is bad for consumers. Among other things, the initiative would make it more difficult for insurance companies to do their preferred thing: focus on reasons for saying no by investigating and denying "suspicious" claims without risking a lawsuit.

The flyer declares further that insurance companies would have to spend more money fighting arguable claims thereby having to raise our rates.

"Arguable claims?"

Consumers Against Higher Insurance Rates seem to be assuming that there is no such thing as an arguable claim; that ALL insurers have nothing but the highest good of the consumers in mind and would never deny a claim arbitrarily nor place their own self-interest above that of their customers.

Right?

Isn't this like saying insurance companies should not be accountable for their self-serving decisions; that if held accountable, they will raise their rates and ask consumers to pay for the consequences of greedy, self-serving and possibly frivolous decisions?

Isn't that economic extortion?

The current remedies now touted by the money opposing R-67 insist that we don't need the initiative because "Washington's consumer protection laws already are among the strongest in the nation."

These laws consist of the dissatisfied entering the world of the state bureaucracy to file complaints with the Insurance Commissioner as well as filing claims under the Consumer Protection Act.

No doubt the Anti's insist that the time to process such claims and complaints would be very short and not harm specific Washington citizens in urgent need.

At least that's the assurance Anti R-67ers want us to believe.

Well, if those processes and procedures are so dang effective, why are we even being asked to vote on a ballot initiative in the first place?

It seems that in this venue, SOMEBODY is being frivolous about the genuine concerns driving R-67.

I read my current Voter's Pamphlet this morning to see who is talking about frivolous lawsuits.

The Explanatory Statement doesn't mention frivolous lawsuits.

The Statement For Referendum Measure 67 doesn't mention frivolous lawsuits.

The Statement Against Referendum Measure 67 mentions frivolous lawsuits eight times, three in the first paragraph.

Shades of Mr. Luntz of "death tax" fame! Do we need to learn more about framing, catch phrases and seriously misstated talking points? Might there be a tomfoolery brainwashing attempt on out-of-touch old codgers who live on Willapa Bay?

So which team ya gonna yell for?

According to the Voters Pamphlet, the all-stars playing on the R-67'ers team include:

- the Washington State legislature (who certain political and economic lobbyists consider to be the ultimate frivolists.)

- Among the more frivolous characters on this legislature team are the Chairs of the House Financial Services Consumer Protection Committee and House Environmental Health Committee.

- The President of SEIU 1199 (that's a Union whose primary goal is advocacy and protection of citizens, especially working class citizens). Now that's a frivolous pre-occupation eh?

- The frivolous Government Relations Director of Northwest Paralyzed Veterans. Paralyzed Veterans? Well don't that beat all? Who would expect frivolity from paralyzed veterans? How COULD they be "given to trifling or undue levity: as in a frivolous, empty-headed person.?"

- The President of the Washington State Council of Firefighters. Aw hell, everybody knows that firefighters don't do anything all day but be frivolous.

- The Director of the Alliance for Retired Americans. What a frivolous joke. Retired Americans are so loaded with cash, any attempt to cut their own medical costs is certainly frivolous .

The all-stars for the "Reject 67'ers" include:

- The President of the Washington State Medical Association whose website says that

The WSMA is a private, non-profit membership organization for physicians. We are funded by physician membership dues, not by the state. The WSMA works on behalf of our members and their patients to provide educational seminars, physician advocacy efforts, lobbying and other services.

Nothing frivolous about who they're worried about. Of course I have to admit that there's nothing frivolous at all in that paragraph about worrying about patients and patients' ability to pay. - The President of the Washington Association of Business whose website says that

AWB speaks for Washington businesses

Nothing frivolous about who they're worried about. Of course, I have to admit, that there's nothing frivolous at all in that paragraph about worrying about workers' ability to pay for insurance.

With a diverse membership consisting of businesses large and small, urban and rural, and from all parts of the state, the Association of Washington Business lobbies in Olympia for public policy that encourages economic growth, boosts productivity and creates jobs. - The President of the Professional Insurance Agents of Washington (PIA Washington/Alaska) whose website asks:

"How is it going to look when those coming to the state either pay rates that are outrageously high or cannot get insurance at all because this law has chased away all of the insurance companies?"

Well, I used to be a professional insurance agent (six years) and in order to stay in business I needed my insurance company that stayed in business by investigating suspicious claims, looked for ways to deny and kept me employed. Nothin frivolous about that. - Washington State Director, National Federation of Independent Business whose website says

While big labor can just take money from union dues to fund political operations, NFIB depends on the generosity of its members to make voluntary contributions in financial support of the organization's political operations.With those contributions, NFIB's SAFE Trust PAC supports proven business candidates who have committed to keeping small business in business.

Now, I of course want to see small business stay in business. In fact, I want to become a small business owner. But what I don't understand is how small businesses paying constantly rising insurance rates can prove that consumer frivolity is the reason for callous and irresponsible insurer behavior in looking for ways to say no. - Executive Director, Liability Reform Coalition whose website says they're

"Committed to Ending Lawsuit Abuse."

Get a load of LRC's Board of Directors:

Attorney At Law (Not a self-interested trial lawyer I'll bet)

Weyerhaeuser Company Vice President of Government Affairs and Corporate Contributions (Contributions? To whom?)

Mr. -------, State Farm Insurance, Sacramento, CA 95814 (Sacramento? California? I wonder what non-frivolous interest he has in Washington State Initiatives)

Leadership Council, National Federation of Independent Business

Yakima Valley Memorial Hospital

Group Health Cooperative

LMN Architects

Washington State Medical Association

Avista Corporation Director, Government Relations

Retired physician (who ran for State Representative as a Republican in 2004 and said that "After 30 years in medicine, ------ knows that we must free patients and doctors from the cost of frivolous lawsuits." Secretary of State Voters Guide

SAFECO Corporation

Liability Reform CoalitionNot a patient advocate in the lot. Lot's of big players but nobody advocating for the little guys.

- President, Washington Construction Industry Council. Couldn't find WCIC via google but I did find this same individual in the voter's pamphlet listed as the Executive Director of the American Council of Engineering Companies of Washington whose website has an icon - Reject R-67 - that when clicked takes you to those guys who sent me the flyer: Consumers Against Higher Insurance Rates.

Click on the link to see the long list of businesses and associations worried about how much insurance you pay. The list of individuals might include someone you know.

Apparently R-67 would not he good for business and what would not be good for business would not be good for Washington right?

Well, at sixty one, I'm fighting off retirement cause my wife and I need the medical. Under the current system in which insurers have constantly raised the rates regardless of frivolity, I've been notified that when I retire, my monthly insurance premium payment will be $893.

That's about the size of my mortgage payment which , when combined with that same non-frivolous insurance premium that presumably protects my wife's and my health, will probably effectively suck up the entirety of my employment-based retirement.

There's of course Medicare about which I haven't changed my mind since February 16, 2006.

Course living on Willapa Bay I can find plenty of wood to burn for heat and light so reasonably I can pay insurance premiums without worrying about utility bills. (But those who don't appreciate my writing will have their day when I can no longer write online, eh?)

Since I won't need the car I can't afford to insure and won't have any way to drive to the hospital for medical treatment, I might as well concede to the Anti-R 67er's, sell the house, sell the car and move to the streets of South Bend where the hospital is just up the hill.

Unless I'm too decrepit, I can walk up that hill myself rather than pay for the ambulance my insurance company won't cover.

How can I be so frivolous about all this?

It really isn't a matter of frivolity is it?

what would you do?

Leave things the way they are with insurers having unlimited ability to raise premiums based on lies about non-existent or a minimal number of frivolous lawsuits?

That sure as hell won't lower my insurance premiums will it?

It sure as hell is no guarantee - based on current insurer denial behavior (whether you've seen Sicko or not) - that any particular coverage I might need will be there in the true spirit of community-shared risk.

Personally, as a life-entrepreneur who earnestly desires to pay as I go and get what I pay for, I'd rather direct the extortion in the opposite direction and tell the insurers,

"You've denied one claim too many. You and your medical associations have used human pain as a weapon of extortion one time too many.

Now - in court if necessary - you'll have to explain yourselves and if you're no good at explanations, you'll pay."

If, as the silly flyer from Consumers Against Higher Insurance Rates warns, rates could increase as much as $205 a year for a typical Washington family, that would be $17.08 per month.

You know, I would gladly add that much to my retirement premium of $893 just to poke the lying insurers in the eye; to see them suffer - even just one time in court - a dose of wallet pain equal to what we live with.